")

Ramesh K. Dhital, FCA

Over the last ten years, NFRS Implementation in Nepal has been a gradual but transformative journey, each phase bringing new complexities with little chaos. The industry debated impairment models, navigated the ECL era where some institutions implementing software while others battling spreadsheets even Effective Interest Rate (EIR) calculations, and addressing regulatory reserve requirements. Lease accounting suddenly meant even rented premises had to sit proudly on the balance sheet, staff loans were adjusted at fair value, and in a few cases, asset revaluations made balance sheets look healthier overnight. Business combinations followed with their practical challenges, including tax disputes over bargain purchases that even reached the courts. IFRS 17 in insurance sector is now bringing intensive trainings, complex actuarial models, and renewed professional excitement. Chartered Accountants welcomed the challenge, industries were occasionally baffled, and investments in systems, consultancy, and compliance helped Nepalese entities strengthen capabilities and align with global best practices.

As a consultant, we enjoyed learning from scratch and assisting clients through these transitions, gaining hands-on experience and seeing first-hand how standards reshape the way businesses report and operate.

And just when we were catching our breath IFRS 18 has landed.

As Nepal moves steadily towards convergence with IFRS 18 – Presentation and Disclosure in Financial Statements, the preparedness of sectoral regulators has become as critical as that of reporting entities themselves. While IFRS 18 primarily reshapes how financial performance is presented and explained rather than what is recognised or measured its successful implementation depends heavily on whether regulatory reporting frameworks evolve in parallel.

Sectoral regulators such as Nepal Insurance Authority, Nepal Rastra Bank prescribe industry-specific reporting formats, prudential returns, and disclosure templates for regulated entities. These formats are often highly prescriptive and, in their current form, may not be immediately compatible with the structural requirements of IFRS 18, particularly in relation to:

• Mandatory categories in the Statement of Profit or Loss

• Defined subtotals such as operating profit

• Enhanced aggregation and disaggregation principles

• Disclosure and reconciliation of management-defined performance measures

The absence of coordinated and harmonised regulatory guidance between accounting standard-setters and sectoral regulators risks creating a regulatory enforcement gap during the transition to IFRS 18. Such a gap can result in interpretative uncertainty, parallel reporting expectations, and an additional compliance burden for banks, financial institutions, listed entities, and other regulated companies that must comply simultaneously with IFRS-aligned financial statements and regulator-mandated formats.

If left unaddressed, this misalignment may undermine the very objectives of IFRS 18 comparability, transparency, and consistency and expose preparers and auditors to heightened compliance and supervisory risk. Early and proactive engagement by regulators is therefore not optional; it is essential.

Understanding IFRS 18

In April 2024, the International Accounting Standards Board (IASB) issued IFRS 18, Presentation and Disclosure in Financial Statements, replacing IAS 1 (NAS 1 in Nepal), Presentation of Financial Statements. IFRS 18 represents one of the most significant changes to financial reporting in recent years and will be effective for annual reporting periods beginning on or after 1 January 2027, with early adoption permitted.

Importantly, IFRS 18 does not alter the recognition or measurement principles of transactions. Instead, it fundamentally reshapes how financial performance information is structured, presented, and explained within general-purpose financial statements. The standard responds to long-standing concerns from investors and analysts about inconsistent presentation of performance and excessive use of entity-specific subtotals.

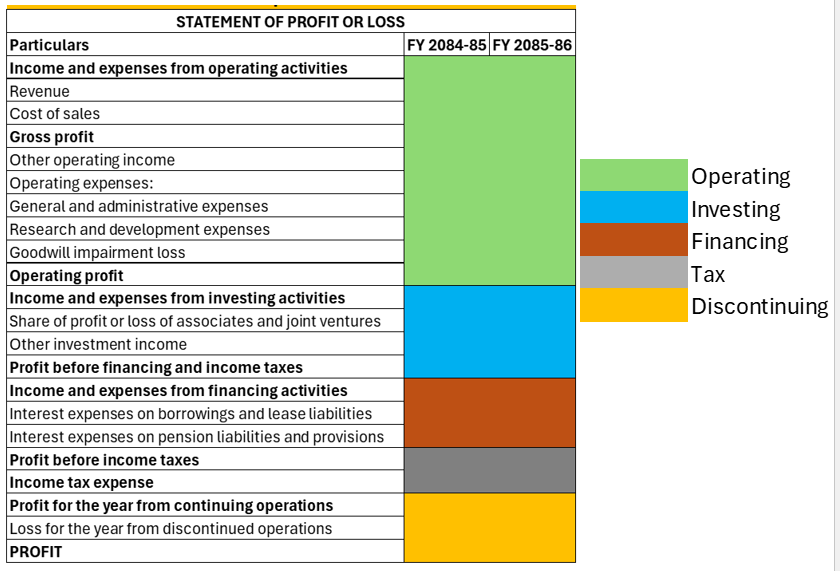

Structured Statement of Profit or Loss

IFRS 18 introduces a mandatory structure for the Statement of Profit or Loss, requiring income and expenses to be classified into operating, investing, financing, income tax, and discontinued operations. It also mandates key subtotals, including operating profit or loss and profit or loss before financing and income tax, significantly improving comparability. This marks a clear departure from the flexibility under NAS 1, where entity-defined subtotals often reduced consistency across financial statements.

Aggregation, Disaggregation, and MPMs

The standard strengthens aggregation and disaggregation principles, discouraging excessive use of broad “other” categories and requiring clearer presentation of performance drivers. IFRS 18 also formally introduces Management-Defined Performance Measures (MPMs) into audited financial statements, requiring disclosure in a single note, explanation of their relevance, transparent calculation, and reconciliation to IFRS-defined subtotals bringing greater discipline and transparency to performance reporting.

Comparability, Credibility in Financial Reporting

As Nepal’s financial sector becomes increasingly integrated with regional and international markets, IFRS 18 enhances the credibility and comparability of financial statements by aligning performance presentation with global best practices. Although primarily a presentation standard, IFRS 18 has meaningful operational implications, including changes to financial statement formats, internal reporting systems, comparative information, and disclosure processes. Entities that delay preparation risk compressed implementation timelines and higher compliance costs.

Nepal Towards IFRS 18

Nepal Financial Reporting Standards (NFRS) are designed to be converged with IFRS Accounting Standards issued by the IASB. As Nepal continues updating NFRS in line with recent IFRS pronouncements, it is expected that IFRS 18 principles will be incorporated into the local reporting framework in due course.

However, convergence at the standard-setting level alone is insufficient. Without parallel regulatory alignment, preparers may face conflicting expectations particularly where regulator-prescribed formats override IFRS-compliant presentation.

The Critical Role of Sectoral Regulators

The transition to IFRS 18 requires active leadership from regulators, including:

• Reviewing and revising prescribed financial statement formats

• Allowing flexibility for IFRS-compliant presentation where appropriate

• Issuing coordinated implementation guidance in collaboration with standard-setters

• Providing transition reliefs or phased adoption where necessary

Regulators play a decisive role in ensuring that IFRS 18 adoption in Nepal is consistent, enforceable, and credible, rather than fragmented and compliance-driven.

Lastly

IFRS 18 marks a fundamental shift in how financial performance is communicated. For Nepal, it presents both an opportunity and a challenge. While preparers and auditors must adapt systems and processes, sectoral regulators must act early to align regulatory reporting frameworks with IFRS 18 principles.

A coordinated approach bringing together standard-setters, regulators, preparers, and auditors will be essential to ensure that the transition to IFRS 18 strengthens, rather than complicates, Nepal’s financial reporting ecosystem.

Ramesh K. Dhital can be reached at [email protected]. This article was originally published in the latest issue of Businesspana Quarterly Magazine.